Compliance in insurance is no longer just a regulatory checkbox; it’s a business imperative for insurers aiming to protect reputation, reduce risk, and foster customer trust.

This blog outlines how compliance in insurance and standards operates, the essential components for success, and seven proven methods to achieve them effectively.

We also highlight real-world use cases, technological innovations, and how Convin’s Agent Assist empowers insurance teams to simplify compliance and maintain regulatory confidence in an ever-evolving landscape.

Compliance in insurance ensures insurers meet regulatory standards, avoid legal risks, and maintain trust. It involves policies, processes, and technology to align operations with evolving industry regulations and customer expectations.

Ensure compliance in insurance with Convin’s Agent Assist

What is Compliance in Insurance and How Does it Work?

In the insurance sector, regulatory compliance and standards ensure that companies operate within legal frameworks and adhere to established industry norms, safeguarding the interests of policyholders and maintaining market stability.

This is how it works,

- Adherence to laws and regulations governs insurance operations, ensuring fairness, transparency, and financial integrity.

- Challenges in keeping up with changing regulations necessitate continuous monitoring and compliance strategy adjustments.

- Compliance is integrated into all aspects of an insurer's operations, from customer interactions to data management.

- Regulatory compliance is the overarching framework companies follow, encompassing adherence to laws, regulations, and guidelines set by regulatory bodies.

- Compliance is central to the insurance business model, influencing decision-making, product development, marketing strategies, and customer service.

- Staying informed about compliance and regulation news is crucial for companies to adapt to changes.

- Real-world compliance examples guide industry best practices.

- Regulatory compliance requirements detail specific mandates for business conduct, risk management, and policyholder protection.

Through this multi-faceted approach, the insurance sector ensures that companies operate responsibly, maintain financial solvency, and offer fair and transparent services to their customers, reinforcing the sector's credibility and trustworthiness.

Only 13% of legal and compliance leaders feel confident that they can manage cross-functional risks without creating drag on the business. - Gartner

Key Components for Successful Compliance in Insurance

The insurance sector operates under a microscope of regulatory scrutiny, where compliance with laws and regulations is not just a legal obligation but a cornerstone of market integrity and consumer trust.

To ensure successful compliance and standards in the insurance sector, companies must focus on these major components:

- Understand Regulatory Compliance Requirements: Continuously update and educate on the latest regulatory requirements to ensure alignment with industry standards.

- Integrate Compliance into Operations: Embed regulatory compliance seamlessly into everyday business operations, ensuring it's a core aspect of the company culture.

- Stay Updated with Compliance News: Monitor compliance and regulation news and updates regularly to stay informed and responsive to changes in the sector.

- Align Compliance with Business Strategy: Ensure compliance and regulatory considerations are integral to the business strategy, underscoring their importance across all business decisions.

- Invest in Technology and Training: Leverage technology for compliance efficiency and provide continuous training to staff, ensuring they know compliance requirements and best practices.

By focusing on these critical components, insurance companies can maintain high regulatory compliance standards, safeguard their reputations, and ensure long-term success in the industry.

Resolve compliance issues faster with Convin’s insights

This blog is just the start.

Unlock the power of Convin’s AI with a live demo.

7 Proven Methods to Achieve Compliance in Insurance

Navigating the complex landscape of regulatory compliance and standards in the insurance sector is critical for industry players.

.webp)

This article discusses seven strategies for insurance companies to adhere to regulations and maintain high compliance standards, ensuring competitiveness in a highly regulated market.

1. Stay Informed on Compliance and Regulation News

Keeping up-to-date with the latest compliance and regulation news is foundational. Regulatory frameworks in the insurance sector are constantly evolving, and what was compliant yesterday may not be compliant today.

Companies should have a dedicated team or resources focused on tracking and interpreting the latest compliance with laws and regulations, regulatory compliance examples, and significant shifts in the regulatory landscape.

2. Implement Comprehensive Training Programs

Training is critical to ensuring that all employees, from the top down, understand the importance of compliance and regulation in business.

Regular training sessions can help staff stay current with the latest regulatory compliance requirements and understand their roles in maintaining compliance. This allows them to adhere to the law and instills a culture of compliance within the organization.

3. Engage in Regular Audits and Assessments

Regular audits and assessments help identify potential regulatory and compliance issues before they escalate. These audits should be thorough and cover all aspects of the business, from operations to data handling.

Identifying and rectifying gaps early can save a company from fines, legal issues, and reputational damage.

4. Leverage Technology for Compliance and Regulation in Operations

Numerous technological solutions are designed to assist with regulatory compliance in today's digital age.

These systems can help automate the tracking of regulatory changes, manage compliance documentation, and ensure that internal processes are aligned with current regulatory requirements. Investing in such technologies can significantly reduce the risk of non-compliance. For distribution-focused insurers, dedicated platforms now automate producer licensing, appointment management, and multi-state compliance tracking, as outlined in one comparison of leading platforms, While also supporting long-term compliance through insurance data archiving.

5. Develop a Robust Compliance Framework

A well-structured compliance framework can provide a clear roadmap for meeting regulatory compliance requirements. This framework should outline the company's roles and responsibilities, define compliance processes, and establish procedures for monitoring and reporting.

Having a solid framework in place ensures that compliance is an integral part of the business strategy.

6. Encourage Open Communication

Create an environment where employees feel comfortable reporting potential compliance issues. Open communication is often the fastest way to identify and address potential problems before they become significant.

Encouraging a culture where compliance and regulation are openly discussed can also lead to better solutions and more innovative approaches to compliance.

7. Stay Proactive with Compliance and Regulation in Business

Being proactive rather than reactive regarding compliance can set a company apart in the insurance industry. This means following current regulations, anticipating future changes, and preparing accordingly.

Staying ahead of the curve can provide a competitive advantage and demonstrate to customers and regulators that the company is committed to the highest standards of compliance and ethical operation.

Insurance companies can navigate regulatory compliance by staying informed, training staff, conducting audits, leveraging technology, establishing a compliance framework, promoting open communication, being proactive, building trust, and ensuring long-term business success.

Stay audit-ready with Convin’s compliance documentation.

Regulatory Compliance in Insurance: Real-Time Use Cases and Innovations

Insurance use cases reflect the innovative applications of technology and data analytics in the insurance industry, offering customers more immediate and interactive services.

Here are some from the insurance sector:

- Telematics in Auto Insurance

- Usage-Based Insurance (UBI): Insurers use telematics devices installed in vehicles or smartphone apps to monitor driving behavior in real-time. Safe driving habits can lead to lower premiums or rewards for the driver.

- Real-Time Risk Assessment: Insurance companies assess risk based on real-time data on speed, braking patterns, and driving hours, allowing for more accurate premium pricing.

- Health Insurance Wearables

- Fitness Tracking for Premium Discounts: Health insurers offer wearable devices to track physical activity, sleep patterns, and vital signs. Policyholders engaging in healthy behaviors can receive premium discounts or rewards.

- Real-Time Health Monitoring: Insurers use data from wearables to offer personalized health advice or early warnings about potential health issues, potentially reducing the need for costly medical interventions.

- On-Demand Insurance

- Temporary Coverage: Apps allow customers to activate and deactivate insurance coverage in real-time for specific items or events, offering flexibility and cost savings.

- Travel Insurance Activation: Travelers can purchase insurance instantly from their mobile devices, obtaining coverage that begins immediately, even if they're already at the airport or en route to their destination.

- Real-Time Claims Settlement

- Instant Claims Processing: Advanced algorithms and AI can assess specific insurance claims in real-time, enabling instant payouts for straightforward claims and enhancing customer experience.

- Photo-Based Claims: In auto insurance, for example, policyholders can submit photos of vehicle damage via an app, allowing insurers to assess and respond to claims rapidly.

- Interactive Customer Service

- Chatbots and AI Assistants: Insurers use AI-powered chatbots to provide real-time assistance, policy information, and claims reporting services, offering 24/7 customer support.

- Virtual Health Assistants: In health insurance, virtual assistants can offer immediate health advice, schedule appointments, or guide policyholders through wellness programs.

These real-time use cases illustrate how the insurance industry is leveraging technology to offer more dynamic, personalized, and efficient services, transforming traditional models to meet modern consumer expectations.

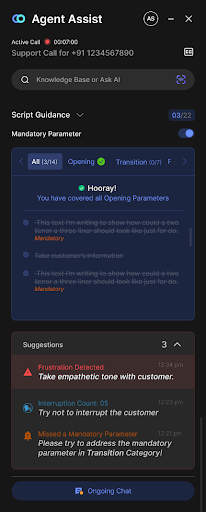

Leveraging Convin’s Agent Assist for Compliance in Insurance

Convin provides AI-driven insights and analytics for sales calls and can play a significant role in helping insurance companies meet regulatory compliance and standards, especially when integrated with an Agent Assist tool.

Here's how Convin's capabilities can be leveraged to enhance compliance in the insurance sector:

1. Real-Time Guidance and Monitoring: Convin's agent assist tool provides real-time guidance to agents during customer interactions, ensuring compliance with regulations and reducing non-compliance risk by monitoring conversations in real time.

2. Real-time Coaching: Agent assist tools to enhance skill enhancement by identifying areas needing training to comply with laws. In contrast, insights from agent interactions ensure a uniform understanding of compliance requirements.

5. Enhanced Supervisor Oversight: Convin helps insurance companies monitor compliance trends, identify improvement areas, and maintain regulatory compliance. It alerts managers to potential breaches or emerging trends, ensuring corrective action.

Supervisor Assist enables real-time tracking of agent performance and active calls, with live notifications sent to managers for violations. It also includes negative sentiment tracking through a live sentiment graph for supervisors and violation alerts.

By leveraging Convin's agent assist tool, insurance companies can ensure that their agents consistently adhere to regulatory compliance and standards, enhancing their reputation, reducing the risk of penalties, and improving overall operational efficiency.

Reduce regulatory risks with Convin’s automated alerts!

Navigating Insurance Compliance with Confidence

Regulations are the backbone of operational integrity and customer trust, and embracing advanced technologies like Convin's agent assist has become not merely a choice but a requirement.

By integrating AI-driven tools, insurance companies can ensure they meet and exceed regulatory compliance standards, safeguarding their reputation and fostering trust with their clients.

The journey toward enhanced compliance is ongoing, and with Convin's Agent Assist, your organization can stay ahead of the curve and adapt to regulatory changes with agility and precision.

Don't let regulatory compliance be your bottleneck. Embrace innovation and transform compliance into your strategic advantage.

Reach out today for an interactive demo and discover how we can tailor our solutions to your unique compliance needs and set a new standard for regulatory excellence in the insurance sector.

Frequently Asked Questions

1. What does compliant mean in insurance?

In insurance, compliance means following all regulatory rules, industry standards, and internal policies, such as proper documentation, disclosures, consumer protection laws, and filing requirements.

2. What are the 4 phases of compliance?

The four common phases are:

- Identify regulatory requirements

- Implement necessary policies and controls

- Monitor ongoing activities and risks

- Report & improve based on findings

3. What are the 5 steps to compliance?

The five steps generally include:

- Assess risks and regulations

- Develop policies

- Train employees

- Monitor & audit compliance

- Correct & update issues

4. What are the 7 pillars of compliance?

The seven pillars usually refer to:

- Leadership & governance

- Risk assessment

- Policies & procedures

- Training & communication

- Monitoring & auditing

- Reporting & investigation

- Corrective action & continuous improvement

5. What are the three types of compliance?

The three common types are:

- Regulatory compliance – following government laws and industry regulations.

- Corporate (internal) compliance – following internal company policies and standards.

- Third-party compliance – ensuring vendors and partners meet required rules and guidelines.

6. What is insurance regulatory compliance?

Insurance regulatory compliance means adhering to laws set by insurance regulators—covering licensing, product filings, claims handling, customer disclosures, solvency rules, data protection, and anti-fraud measures—to ensure fair, transparent, and lawful insurance operations.

.avif)

.avif)