The renewal desk was built to collect, not expand. Every day, thousands of policies renew quietly, without a single conversation about rider upgrades or added protection.

Yet, the same insurance renewal process can be a goldmine of expansion opportunities when powered by timing, data, and AI cadence.

Renewal teams often operate like collection agencies, chasing payments, sending reminders, and closing the file once the policy is paid. But the post-renewal silence costs more than missed premiums; it erodes wallet share.

Studies show that many insurers send renewal reminders just 2–4 days before renewal, which is considered late compared to best practices that recommend at least 14 days’ notice.

These workflow gaps lead to lapsed policies, manual chases, and unhappy customers.

The truth? The gap isn’t intent, it’s timing. Automation and policy renewal automation tools can identify eligibility, nudge at the right moment, and turn passive renewals into micro-sell moments. In other words, the next big upsell might just be hidden in your renewal cadence.

See how leading insurers are turning renewals into upsell opportunities with Conivn

Why the Insurance Renewal Process Still Focuses on Collection, Not Growth

Walk the floor of any renewal desk, and you will see the same loop. Batch reminders, payment chases, and files closed once the premium lands. The insurance renewal process is built to prevent lapse, not to grow coverage.

That loop quietly drains revenue. Renewal teams send out reminders in batches, sometimes days late, and one in three customers hears about their due date when it’s already at risk of lapsing. By then, the focus shifts to recovery, not relationship.

Meanwhile, 40% of inbound leads never get a follow-up, which means those same customers don’t get re-engaged when renewal time comes around. They fall through the cracks, not because agents don’t care, but because the system doesn’t nudge them in time.

And here’s the silent killer: only about 2% of sales calls ever get reviewed. So the insights, the missed cues, the upsell openings, they’re all hidden in unlistened calls. No feedback, no coaching, no improvement.

In short, every delay, every unreviewed call, and every missed follow-up turns a renewal opportunity into a lost conversation. And that’s what keeps policy persistence flat, even when teams are working harder than ever.

Why does it keep happening?

- Renewal KPIs reward collection rates, not coverage expansion.

- Agents don’t see which customers are eligible for rider upgrades.

- Tools still trigger renewal reminders on dates, not on life events or eligibility windows.

So even the best-performing renewal desk ends up running a high-effort, low-yield loop. Reminders go out late. Follow-ups pile up. And while policies get renewed, revenue per policy stays flat.

The irony? These are the customers who’ve already said “yes” once. They’re warm, known, and willing, but the workflow isn’t built to talk to them beyond a payment confirmation.

When renewals are reduced to a transaction, two things happen:

- The customer sees no reason to stay loyal next year.

- The insurer keeps fighting for new business instead of expanding the base they already owns.

The result: more marketing cost, higher churn risk, and untapped rider revenue left sitting in the CRM.

Run a quick audit of your renewal workflows to spot missed upsell opportunities.

What a Modern Insurance Renewal Process Should Look Like

The best renewal conversations don’t sound like transactions; they sound like care.

Instead of “Your payment is due,” imagine an agent saying, “It’s been a year since you started this policy, anything new we should protect?”

That’s what renewal done right looks like.

In a modern insurance renewal process, automation doesn’t replace agents; it empowers them. Renewal reminders go out early, not urgently. Grace-period calls happen on time, not in panic. And when a customer picks up, the system already knows their profile, eligibility, and open service tickets, setting the stage for a real conversation, not a cold script.

Agents don’t have to guess when to pitch a life insurance rider; eligibility-aware prompts tell them who’s ready, when, and why. It’s proactive, not pushy.

Meanwhile, QA transforms from random spot-checks into total visibility. With 100% call coverage through auto-QA, every interaction is reviewed, every missed upsell cue is flagged, and every compliance slip is corrected before it turns into a pattern. Coaching stops being reactive; it becomes continuous.

And because renewals don’t exist in a vacuum, proactive claims status updates play their part too. When customers aren’t left waiting for claim updates, complaint volumes fall, trust rises, and renewal conversations happen on warmer ground.

What starts as smoother claims handling ends as stronger persistency, the kind that makes upsells feel natural, not forced.

That’s the quiet revolution of renewal done well: consistency, confidence, and conversations that grow relationships, not just collections.

Watch a 2-minute demo of how automated renewal cadence and rider prompts create more human conversations.

This blog is just the start.

Unlock the power of Convin’s AI with a live demo.

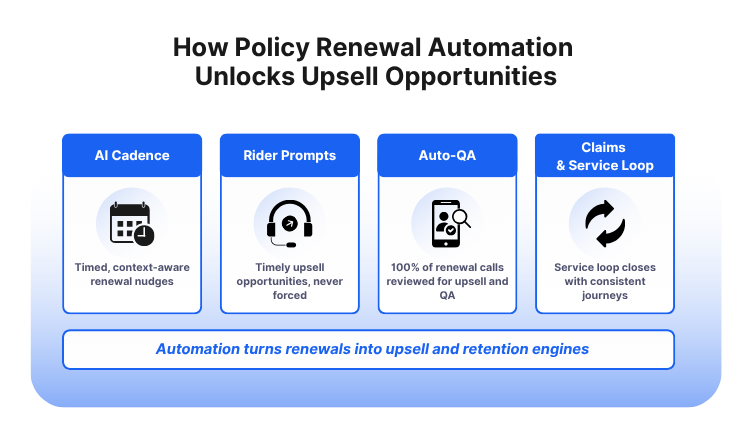

How Policy Renewal Automation Unlocks Upsell Opportunities

Every insurer talks about “customer centricity,” but only a few build it into their renewal DNA. That’s where automation stops being a buzzword and starts becoming a bridge, connecting timing, eligibility, and empathy.

Convin’s renewal automation isn’t about sending more reminders; it’s about sending the right one, at the right moment, with the right context.

1. AI cadence that adapts to the customer

No more batch-driven renewal lists. Convin’s cadence engine schedules renewal, grace-period, and reinstatement calls exactly when engagement is most likely. Each call or WhatsApp nudge carries the customer’s policy context, so outreach feels informed, not repetitive.

2. Rider prompts that surface real opportunities

During every renewal conversation, eligibility-aware prompts appear right in the agent’s flow, not buried in CRM tabs. If a customer qualifies for a life insurance rider or add-on, the system nudges the agent mid-call, ensuring upsell pitches are timely and relevant, never forced.

3. Auto-QA that ensures every call counts

Convin’s auto-QA reviews 100% of renewal and sales interactions, surfacing missed upsell cues, compliance gaps, and training needs. Instead of random audits, renewal managers see patterns: which objections derail conversions, which scripts drive acceptance, and where to coach next.

4. Closing the loop with claims and servicing

Renewal persistence improves when the journey stays consistent. Convin’s AI agents also handle claim updates and follow-ups, keeping customers informed and reducing complaint spillover into renewal season. A cleaner service loop equals a warmer renewal desk.

Together, these workflows turn the insurance renewal process from a chase into a cadence, one that quietly grows renewal rates and customer value in tandem.

Watch a 2-minute demo on AI renewal prompts and see how eligibility-aware offers fit into your existing stack.

Proven Results of Renewal Automation in Insurance

Data tells a simple story, when renewals stop being mechanical, revenue starts compounding.

Across the insurance world, the shift is already underway. The Society of Actuaries’ 2024 report shows that carriers modernizing renewal outreach with event-driven journeys are sustaining 13-month persistency near 83 %, a level that used to be reserved for the top 5% players. Renewal success isn’t about luck anymore; it’s about timing.

Quality assurance follows the same pattern. Most renewal desks used to review only 2–4 calls per agent per month, which meant 95 % of customer conversations went unheard. Now, with 100 % call visibility through auto-QA, missed upsell cues and compliance slips are no longer invisible; they’re fixable, fast.

And customer experience? It’s where the real differentiation begins. Capgemini’s 2024 Life & Health report found that only 5 % of carriers deliver “best-in-class” experiences, almost all of them those that connected claims, servicing, and renewal loops into a single cadence.

That closed loop builds trust long before the next premium reminder.

Convin’s own results mirror that industry story in sharper detail:

- 35 % improvement in renewal collection within three months of automating workflows.

- 40 % fewer complaints once AI agents handled claim status updates proactively.

- 10× jump in conversions when cadence became contextual, not calendar-driven.

(Source)

These aren’t isolated pilots; they’re renewal teams working with the same headcount and systems, simply powered by smarter cadence, eligibility-aware prompts, and always-on QA.

The outcome is consistent: higher persistency, cleaner compliance, and upsell conversations that feel natural, not tactical.

Get a benchmark snapshot of your QA coverage vs. peers and see where your renewal process stands today.

7-Step Playbook to Automate Policy Renewals and Drive Upsells

Renewal performance improves fastest when teams simplify workflows and sharpen intent.

Here’s how high-performing insurers transform renewals from collection to expansion, one practical step at a time.

1. Redefine what “renewal success” means

Go beyond payment collection as the main KPI. Add upsell conversion, policy expansion, and customer satisfaction to your dashboard. When success is measured by value retained and grown, behaviors align naturally.

2. Design journeys around customer events, not calendar dates

Structure your insurance renewal process to respond to real triggers — T-30, T-15, T-3, grace, and reinstatement. Event-driven reminders and calls start conversations earlier and create space for meaningful discussion, not deadline chases.

3. Expose eligibility at the point of contact

Integrate CRM and policy systems so agents can see rider eligibility and life-stage context during renewal calls. Simple logic rules like “child rider for dependents under age five” or “home loan coverage when mortgage detected” make offers relevant and precise.

4. Equip agents with mid-call intelligence

Insert eligibility-aware prompts directly into the call interface. These guides help agents suggest upgrades or riders naturally, using language that fits each customer profile.

5. Replace random QA with full-coverage insight

Adopt auto-QA to review 100 percent of renewal and upsell calls. Use the insights to coach continuously on missed opportunities and compliance gaps. Quality improves faster when visibility is complete.

6. Strengthen the claim-to-renewal connection

Automate claim-status updates and proactive follow-ups. When customers feel informed and supported through claims, complaint volumes drop and renewal trust rises.

7. Pilot, measure, scale

Test the new cadence with one policy cohort. Compare renewal rate, upsell lift, complaint volume, and average handling time before and after automation. Use results to refine playbooks and secure buy-in for wider rollout.

Incremental improvements in timing, visibility, and coaching compound quickly. Within a single renewal cycle, they translate into higher persistency, better agent morale, and stronger lifetime value per policyholder.

Addressing Concerns About Automated Policy Renewals

Every insurer that modernizes its renewal desk faces a few natural questions. These aren’t signs of resistance; they’re signs of care. The people who keep renewal pipelines running worry about how change will affect customers, compliance, and their own role. Here’s how leading teams have managed those shifts successfully.

1. “Automation will make us sound robotic.”

That worry comes from a good place: no insurer wants to lose the human tone customers expect. In practice, automation does the opposite. When cadence is tuned to each customer’s context and language preference, outreach feels personal because it happens at the right time.

Start with limited triggers. Review early messages weekly and adjust voice or timing. Keep agent-led conversations for high-value renewals until confidence builds.

2. “Compliance risk will rise if AI handles renewals.”

Compliance is never optional, and it shouldn’t depend on memory. Automated cadence and auto-QA bring discipline to every disclosure and consent line. Each reminder, call, and transcript is stored and auditable, reducing the chance of missed statements or human error.

Involve compliance early in workflow design. Tag every disclosure for auto-QA review and keep transcripts stored securely for quick audits.

3. “Agents might resist or feel replaced.”

That concern is genuine; renewal agents have spent years earning customer trust through voice and empathy. Automation can sound like it’s taking that away. In reality, it gives them back the minutes they lose to manual reminders and follow-ups.

Automation covers the routine so agents can focus on what only people can do: read tone, handle emotion, and guide decisions. Many teams that adopted this model describe it as relief, not replacement.

Include agents from day one. Pilot small batches so they experience how cadence removes repetitive work and increases meaningful upsell chances. Let them track their own lift; success speaks louder than change management.

4. “We might overwhelm customers with reminders.”

Too many messages come from static schedules, not from intent. Event-based cadence fixes that by triggering outreach only when renewal, grace, or eligibility windows open. The rhythm follows the customer, not the calendar.

Cap outreach frequency per phase (two pre-lapse reminders, one grace call). Blend channels, voice for priority, WhatsApp or email for gentle nudges.

5. “We don’t have bandwidth for another platform.”

Most insurers start small. Renewal automation integrates with existing CRMs and dialers, so the learning curve stays light. The time saved from manual chases usually offsets rollout effort within a single cycle.

Run a 30-day pilot with one product line. Compare hours spent per renewal and persistency improvement. Use savings and lift data to fund expansion.

Change in renewal operations isn’t about replacing people or process; it’s about freeing both to do their best work. When automation handles precision, people regain presence — and that’s where stronger customer relationships begin.

Watch a 2-minute demo on how leading insurers automate renewals without losing the human touch.

Transforming the Insurance Renewal Process into a Growth Engine

Renewals have always been about retention. But in today’s market, retention alone isn’t enough; it’s the starting line.

Every policy renewal is proof that a customer still trusts you. That’s not a back-office event; that’s a live opportunity. When handled with precision and empathy, that moment can grow coverage, deepen loyalty, and increase lifetime value, all within the same conversation.

The insurance renewal process is no longer just a chase for payment; it’s a test of timing, relevance, and readiness. And automation is what brings those three together.

When cadence handles the reminders, agents can focus on intent. When data reveals eligibility, offers feel personal. When QA covers every call, consistency becomes culture.

That’s how insurers quietly turn renewals into revenue engines, not by adding more tools or people, but by rethinking the rhythm of customer contact.

Change doesn’t have to start big. Start with one renewal workflow, one policy line, and one team. Watch how the right timing and a relevant rider prompt can turn a routine payment into a conversation about protection.

Because when renewal stops being a reminder and starts being a relationship, growth takes care of itself.

Take a 15-minute diagnostic to identify renewal-to-upsell gaps in your process.

FAQ

1. How does upselling increase revenue?

Upselling increases revenue by raising the average value of each existing customer instead of acquiring new ones. In insurance, that means adding riders, top-ups, or higher coverage tiers during renewal conversations.

Here’s how it impacts revenue directly:

- Higher premium per policy: Every rider or add-on increases policy value.

- Improved persistency: Engaged customers with customized coverage are more likely to renew next year.

- Lower acquisition cost: You earn incremental revenue from existing customers without new marketing spend.

In short, upselling grows Customer Lifetime Value (CLV) while reducing Cost to Acquire (CAC). Automation helps identify who’s eligible, when to offer, and how to position it; making upselling both timely and scalable.

2. What is the renewal strategy?

A renewal strategy is the planned approach insurers use to retain customers and expand their coverage during policy renewals.

A strong renewal strategy typically includes:

- Proactive communication: Timely reminders before due dates (T–30, T–15, T–3 days).

- Personalized outreach: Tailored scripts or offers based on the customer’s policy, age, and life events.

- Automated cadence: Scheduled follow-ups across voice, WhatsApp, and email for consistent engagement.

- Eligibility-driven upsells: System prompts when a customer qualifies for an add-on.

- Post-call QA and coaching: Continuous review of calls to improve pitch, compliance, and timing.

Done right, a renewal strategy turns a payment reminder into a relationship moment, securing retention and unlocking expansion in one motion.

3. How to calculate upsell revenue?

You can calculate upsell revenue using a simple formula:

Upsell Revenue=(New Premium after Upsell)−(Original Premium)

Example:

A customer’s base policy premium = ₹10,000

They add a critical illness rider worth ₹2,000 →

Upsell Revenue = ₹2,000

Upsell Revenue % = (2,000 / 10,000) × 100 = 20%

In renewal analytics, aggregate this across all policies in a cycle to get:

- Total upsell revenue per cycle

- Upsell contribution to total premium growth

Tracking these metrics helps renewal teams prove how much value automation and cross-sell cadences are creating.

4. What is the main purpose of upselling?

The main purpose of upselling is to increase customer value while improving customer satisfaction.

In insurance, upselling isn’t about pushing more; it’s about filling protection gaps.

For example:

- Adding a life insurance rider for a growing family

- Offering accident or health riders when new risks appear

- Upgrading term coverage after an income change

The outcome is twofold:

- The customer feels better protected and more loyal.

- The insurer increases average revenue per policy and persistency.

When done right, upselling strengthens both financial performance and customer relationships, making it a win-win.

.avif)

.avif)