In a world where speed and precision are everything, the underwriting engine of life insurers is under pressure like never before. The global life‑insurance underwriting market alone is estimated at $500 billion in 2025 and projected to grow at a 7 % CAGR through 2033.

Meanwhile, Predictive analytics in insurance is no longer a niche experiment; it’s fast becoming the turning point that separates nimble carriers from industry laggards.

What if you could leverage every conversation your applicant ever had, every policy decision ever made, and every behavioural cue captured by the voice‑bot to unlock smarter, faster underwriting?

In this blog, you’ll explore how predictive analytics in insurance is rewriting underwriting for life insurers, combining historical policy data with call transcripts, real‑time voice interactions, agent‑assist triggers, and advanced models.

You’ll walk through an underwriter’s workflow, uncover key use‑cases (including accelerated underwriting life insurance and automated risk assessment life insurance), and see how platforms like Convin power the shift to true data‑driven underwriting decisions.

Turn every policy, call, and signal into underwriting intelligence with Convin AI

The Rise of Predictive Analytics in Insurance

The world of life insurance is shifting fast: traditional underwriting workflows that used to stretch into weeks are under pressure to evolve. According to recent data, the typical life‑insurance underwriting process can take from 24 hours up to 4‑6 weeks, depending on complexity.

That means insurers face mounting expectations to deliver speed, accuracy, and customer‑centric experience.

Enter predictive analytics in insurance, which brings the power of data, machine learning, and automation into the heart of risk assessment. When insurers apply insurance predictive analytics and insurance analytics effectively, they can transition from manual loops to streamlined, responsive decisions.

In the next section, we’ll explore how this plays out specifically for life insurers and underwriting workflows.

- Growing Adoption of Insurance Predictive Analytics

Life insurers are rapidly shifting from rule-based underwriting to model-driven decisioning. Predictive analytics in insurance is central to this evolution.

New data types, like wearables, electronic health records, and behavioural analytics, are now accepted underwriting inputs. Deloitte reports that 70% of insurers already use or plan to use advanced analytics in underwriting to improve risk selection and pricing.

This trend allows life insurers to accelerate application decisions, reduce operational costs, and enhance their customer experience. Predictive analytics in life insurance is becoming standard for competitive growth.

The shift to predictive models is no longer optional; it's essential for scalable underwriting and strategic agility.

- Predictive Analytics in Life Insurance: An Overview

Predictive analytics in life insurance synthesizes diverse data sources to better estimate individual risk and improve decision accuracy.

Models draw from historical policy behavior, lab results, socioeconomic indicators, and voice-based interactions. According to the Society of Actuaries, insurers applying predictive models reported a 10–20% improvement in risk assessment precision.

The use of predictive analytics enables better segmentation, streamlined underwriting, and optimized pricing, cornerstones for accelerated underwriting of life insurance.

By integrating structured and behavioural data, predictive analytics reshapes how life insurers assess and act on risk.

- Shifting from Traditional to Data-Driven Underwriting Decisions

Insurers are replacing manual, time-intensive processes with analytics-driven systems that speed up underwriting.

Traditional underwriting often relies on static data and slow documentation. Predictive analytics in insurance introduces automation through real-time data and decision algorithms. LIMRA notes that digital adoption has cut underwriting times by up to 50% across participating carriers.

This transition enables insurers to prioritize complex cases while automating straightforward ones, ensuring faster and more consistent data-driven underwriting decisions.

Data-driven systems lead to faster approvals, better consistency, and higher underwriting capacity.

As adoption grows, insurers are embedding predictive analytics deeper into operational workflows, especially underwriting.

Start your analytics transformation with Convin AI today

How Insurers Use Predictive Analytics in Underwriting Workflows

Underwriting is no longer just a series of checklists; it’s evolving into a dynamic decision engine. With predictive analytics in insurance, life insurers now merge historical policy data with real‑time conversational inputs (call transcripts, voice interactions) to accelerate and refine risk assessment.

The life‑insurance underwriting market itself is projected to grow robustly, with a $500 billion base in 2025, with a 7 % CAGR through 2033.

That’s why the workflow matters: how data is collected, processed, scored, and then turned into underwriting action is critical.

1. A Typical Underwriting Workflow in Life Insurance

Understanding the current underwriting process highlights why predictive analytics is now indispensable.

The standard process includes applicant intake, medical record review, lifestyle assessments, and risk classification. Many carriers also rely on APS (Attending Physician Statements), which can take weeks to retrieve and analyze. McKinsey found that 30–40% of underwriting costs are tied to manual data gathering.

By using predictive analytics, insurers eliminate redundant steps and replace manual reviews with model-generated scores.

Modernizing workflows with analytics accelerates decision-making and enhances operational efficiency.

2. Combining Policy Data & Call Transcripts via Convin Voice Bot

Integrating historical and real-time customer interaction data can significantly boost underwriting accuracy.

Policy data such as lapse history, premium behavior, and health indicators offer a base layer. Voice bots capture speech patterns, emotion, and hesitation, providing behavioural context. According to IBM, behavioral signals improve model performance by nearly 15%.

By combining these, insurers enhance predictive analytics in life insurance models and reduce dependency on follow-ups or ambiguous disclosures.

Fusing structured policy data with dynamic call insights allows smarter, more responsive underwriting workflows.

3. Workflow Chart: Predictive Analytics in Life Underwriting

A predictive underwriting workflow integrates applicant data, risk scoring, and automated triage in one cohesive system.

Starting from application intake, data flows into a centralized engine that pulls historical, third-party, and interaction-based data. Predictive models assess risk using predefined criteria. Applications are sorted: approved, flagged for review, or declined. Feedback from outcomes loops back to improve future model accuracy. Accenture notes that AI-enabled underwriting can cut cycle time by up to 80%.

This workflow design shows how predictive analytics operationalizes decision-making with agility and precision.

4. Speeding Up Approvals with Automated Risk Assessment Life Insurance

Quick approvals are crucial for applicant satisfaction and conversion.

Predictive analytics in insurance supports instant triage of low-risk applications using AI-based scoring. According to LexisNexis, carriers leveraging automated tools saw a 30% improvement in policy issue times.

Automation also reduces underwriting leakage and allows underwriters to focus on nuanced cases. Automated risk assessment tools enable fast, fair, and scalable underwriting decisions.

Advanced analytics shifts underwriting from static checklists to fluid, responsive systems powered by real-time data.

This integration powers tangible benefits across underwriting, from decision speed to fraud detection.

Build your predictive underwriting workflow with Convin AI

This blog is just the start.

Unlock the power of Convin’s AI with a live demo.

Key Use Cases of Predictive Analytics in Life Insurance

Understanding the rise and workflow is one thing, but implementation is another. Life insurers are leveraging predictive analytics in insurance to unlock specific use cases: accelerated underwriting life insurance, fraud detection, and smarter pricing through insurance analytics.

As they deploy insurance predictive analytics, firms are reporting meaningful improvements in underwriting speed and accuracy. For example, one study noted that simplified underwriting leveraging predictive modeling can reduce turnaround from weeks to days.

1. Accelerated Underwriting Life Insurance: Real-World Impact

Accelerated underwriting has moved from experimental to essential in the insurance ecosystem.

Carriers using predictive analytics in life insurance can streamline application decisions without lab tests. Swiss Re found that 60% of U.S. insurers now issue some policies through accelerated paths.

These policies improve customer satisfaction and drive digital channel growth.

Predictive models make accelerated underwriting scalable, safe, and business-relevant.

2. Detecting Fraud and Reducing Underwriting Leakage

Undetected fraud and process inefficiencies reduce underwriting ROI.

Predictive analytics in insurance can detect subtle anomalies in application behavior and conversation transcripts. According to the Coalition Against Insurance Fraud, insurers lose over $80B annually to fraud.

By embedding fraud scoring into underwriting flows, insurers minimize financial risk and protect portfolio quality.

Fraud detection capabilities enhance underwriting outcomes and long-term portfolio performance.

3. Enhancing Accuracy with Insurance Analytics

Precision underwriting drives profitability and customer alignment.

Insurance analytics refines risk pools and pricing. PwC reports that insurers using analytics-based pricing saw loss ratios improve by 3–5 points. Enhanced accuracy translates into better policyholder retention and lower claims volatility.

Analytics-backed precision strengthens underwriting efficiency and trust. These benefits come to life in targeted applications that drive measurable business outcomes.

Delivering on these use cases depends on actionable, high-quality data, something Convin helps insurers capture and activate.

Launch your accelerated underwriting pilot with Convin AI

How Convin Powers Predictive Analytics in Insurance

Technology is the enabler behind the promise of predictive analytics in insurance. But not all solutions deliver the depth, context, and real‑time integration needed for life‑insurance underwriting.

That’s where Convin’s solutions stand out: combining voice interactions, conversation intelligence, and voice of customer tools with policy‑ and agent‑data to amplify underwriting workflows.

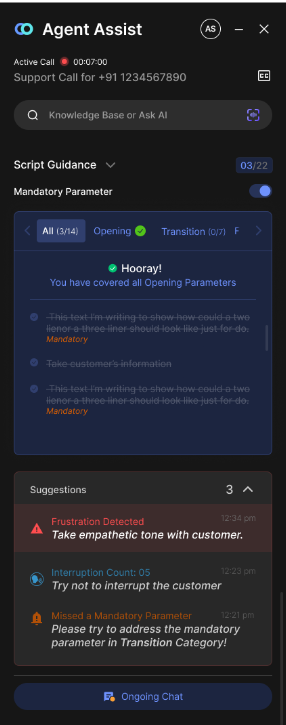

1. Real-Time Agent Assist for Smarter Underwriting

Modern underwriting starts at the point of interaction. Convin’s Real-Time Agent Assist doesn’t just support agents; it transforms customer conversations into structured underwriting signals.

By surfacing prompts, capturing disclosures, and tracking emotional cues live during calls, it feeds relevant, timely data directly into risk models. This improves case accuracy and reduces missing data points that often delay or distort underwriting. The data is clean, contextual, and model-ready.

For life insurers, this means underwriters get complete interaction summaries with pre-tagged insights, accelerating triage, improving compliance, and informing better underwriting outcomes.

2. Voice of Customer and Insurance Predictive Analytics

Beyond words, the way customers speak tells a deeper story. Convin’s Voice of Customer software captures tone, hesitation, satisfaction levels, and behavioral markers in every interaction.

These signals are gold for predictive analytics in life insurance. They offer early indicators of risk, intent, and credibility, complementing traditional policy data. For example, a hesitant tone in answering health-related questions may flag a case for deeper review.

With VoC data enriching predictive models, insurers can refine segmentation, adjust scoring, and personalize underwriting flows to improve both speed and fairness.

3. Conversation Intelligence for Accelerated Underwriting Life Insurance

Accelerated underwriting relies on minimal data. But that data must be deep and rich. Convin’s Conversation Intelligence product ensures every interaction is transcribed, analyzed, and converted into underwriting inputs.

It tags key moments, disclosures, objections, concerns, and aligns them with risk markers. This means even cases that bypass lab work or medical exams can still be evaluated with behavioral depth.

In predictive analytics in insurance, this input expands the model’s accuracy and helps scale accelerated underwriting life insurance programs safely.

Convin’s technology enables predictive models to thrive, enhancing data integrity, context, and decision speed at every step.

Activate agent assist for live underwriting with Convin AI

Predictive Analytics in Insurance is the Future

Predictive analytics in insurance is no longer a future consideration; it’s a current business necessity. For life insurers, underwriting powered by real-time data, behavioural signals, and intelligent models is defining the next wave of growth. From risk segmentation to fraud detection and accelerated workflows, data-driven underwriting decisions are setting new benchmarks for speed, accuracy, and customer experience.

But data alone doesn’t move the dial; how you capture and activate it does. That’s where conversation intelligence, agent assist tools, and voice-of-customer systems come into play.

Platforms like Convin don’t just plug into your workflow; they elevate the quality of your underwriting inputs, giving predictive models the context and clarity they need to perform better, faster.

For executives ready to lead in this shift, the path is clear: transform underwriting into a strategic advantage powered by insurance predictive analytics.

Want to see how this looks inside your own operations? Book a demo today!

FAQ

Q1: What is predictive analytics in insurance underwriting?

Predictive analytics in insurance underwriting uses historical policy data, behavioral signals, and interaction insights to assess risk and automate decision-making. It enables insurers to segment applicants more accurately, reduce manual reviews, and accelerate policy issuance, especially in life insurance.

Q2: What is predictive analytics for decision-making?

Predictive analytics supports decision-making by identifying future outcomes based on past data patterns. In insurance, it helps underwriters, actuaries, and business leaders forecast risk, prioritize actions, and deploy resources efficiently, all while improving customer experience.

Q3: What are the 4 types of analytics?

The four types are:

- Descriptive analytics – What happened?

- Diagnostic analytics – Why did it happen?

- Predictive analytics – What might happen next?

- Prescriptive analytics – What should we do about it?

Q4: What is the main advantage of using predictive analytics in insurance?

The biggest advantage is speed with accuracy. Predictive analytics in insurance streamlines underwriting by enabling faster, data-driven decisions while reducing fraud, risk, and operational costs. Tools like Convin enhance this by enriching model inputs with real-time voice and interaction data.

.avif)

.avif)