Insurance call center cost reduction doesn’t begin with downsizing. It begins with understanding why operational friction keeps rising even when teams work harder than ever.

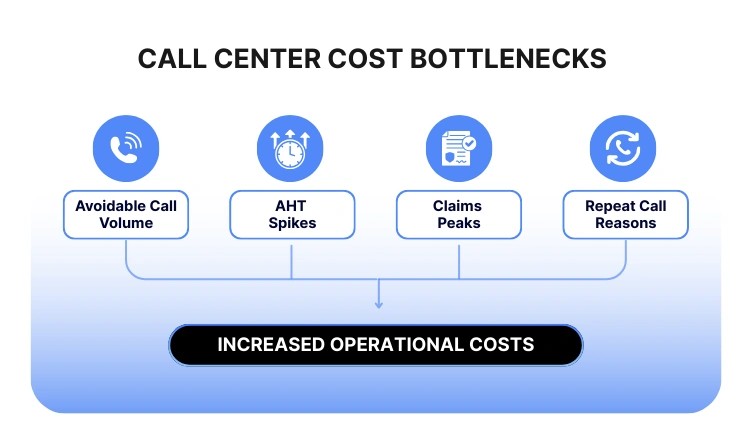

Across the industry, call center cost optimization is becoming difficult because volumes climb faster than support processes can adapt. Claims updates, policy servicing questions, and seasonal surges create avoidable calls that absorb capacity.

At the same time, Average Handle Time (AHT) in many insurance contact centers still spans 7–10 minutes, and FCR often falls below the 70–79% benchmark. When fewer issues are resolved on the first call, repeat traffic becomes an invisible cost driver.

When insurers can see what drives avoidable calls, what slows AHT, and what prevents agents from resolving issues cleanly, cost-to-serve drops naturally. The objective is to eliminate the bottlenecks that drive up service costs, not to lay off employees.

The assurance here is simple: with clearer insight into conversations and operational patterns, insurance call center cost reduction can be steadily worked upon while protecting both service quality and team stability.

See what drives insurance call center cost reduction.

Why Call Center Costs Keep Rising Even When You Add Headcount

On paper, insurance contact centers look well-staffed. New agents are hired, queues are monitored, and service levels are tracked. Yet call center cost optimization remains elusive. Costs climb faster than planned, and leaders still face long AHT, repeat calls, and rising pressure during claims peaks.

The core issue: most insurers are scaling people to manage issues that could be prevented or resolved more efficiently. Let’s unpack the main bottlenecks.

- Rising Call Volumes Quietly Inflate Cost-to-Serve

Most teams feel the impact of rising call volumes in schedules and overtime, not in root-cause visibility.

- What's actually happening: A lot of these calls could have been prevented, such as follow-ups resulting from incomplete resolutions, clarifications regarding unclear communication, or status checks that agents have already provided. As product complexity grows and policies change, customer questions multiply.

- Why this drives cost: Every additional preventable call consumes agent time, adds to Average Handle Time (AHT), and increases the number of full-time employees required to maintain service levels. Cost to serve rises even if nothing else changes.

- What leaders need to see: A clear breakdown of call drivers:

- Which categories are low-value or repetitive?

- Which journeys (claims, renewals, endorsements, FNOL) generate the most repeat contacts?

- Where does unclear communication trigger inbound volume?

When this picture becomes visible, insurance call center cost reduction stops being abstract and becomes a series of specific, fixable workflows.

- Manual QA Covers Too Few Calls to Catch Inefficiencies

Traditional QA was designed for sampling quality, not for understanding systemic inefficiencies.

- What’s really happening:

QA teams typically review a very small percentage of calls, often in the 1–3% range. That may be enough to check tone and compliance on a few calls, but it’s not enough to see patterns in AHT, repeat issues, or process breakdowns. - Why does this drive cost:

- Inefficient call flows remain invisible because they don’t appear in the tiny sample.

- Common agent workarounds (putting customers on hold to navigate slow systems, skipping key probing questions, or over-transferring calls) are rarely captured consistently.

- Corrective actions are reactive and anecdotal.

- Inefficient call flows remain invisible because they don’t appear in the tiny sample.

- What leaders need to see:

- How often do certain failure modes (like incomplete resolutions or unclear explanations) actually occur?

- Which call types routinely exceed target AHT?

- Which teams or processes are most affected?

- How often do certain failure modes (like incomplete resolutions or unclear explanations) actually occur?

Without this visibility, call center cost optimization efforts are based on opinion, not evidence. The result is well-intentioned but misdirected initiatives.

- High AHT Driven by Repetitive, Low-Complexity Queries

Not all long calls are “complex.” Some are just slow.

- What’s really happening:

Repetitive inquiries, such as status updates, straightforward coverage queries, and policy clarifications, take up too much time for agents because:- Systems are slow or fragmented.

- Knowledge is hard to search for in the moment.

- Scripts don’t adapt to real customer language or scenarios.

- Why does this drive cost:

- When Average Handle Time in insurance creeps toward the upper end of the 7–10 minute range, staffing models immediately become more expensive.

- Agents who could handle more complex, value-adding calls are tied up on avoidable repetition.

- Long calls can still result in repeat contacts if the root issue isn’t fully addressed.

- When Average Handle Time in insurance creeps toward the upper end of the 7–10 minute range, staffing models immediately become more expensive.

- What leaders need to see:

- Which call types consistently take longer than expected?

- How much of that time is spent navigating systems vs. actually resolving issues?

- Where do customers ask the same questions again and again?

- Which call types consistently take longer than expected?

Reducing AHT here isn’t about rushing agents. It’s about removing friction so that simple calls stay simple and are resolved the first time.

- Claims Peaks Lead to Overstaffing and Overtime

The stakes are highest, and inefficiencies are most costly when it comes to claims.

- What’s really happening:

Claims-related calls spike during events: storms, natural disasters, premium changes, or product changes. When this happens, most insurers respond with emergency staffing:

- Approving overtime

- Pulling people from back-office roles

- Hiring temporary staff

- Why does this drive cost:

- These decisions are made reactively, often with limited data on call drivers and duration.

- Overtime and temporary staffing carry a premium cost.

- Stress on frontline teams increases errors, which can create even more follow-up calls and complaints.

- These decisions are made reactively, often with limited data on call drivers and duration.

- What leaders need to see:

- Historic patterns of claims call volume by event, line of business, and region

- Which parts of the claims journey (FNOL, documentation, status updates, settlement) generate the highest contact rates

- Where clearer outbound communication or self-service could absorb volume

- Historic patterns of claims call volume by event, line of business, and region

Understanding call drivers around claims allows insurers to manage spikes with more precision, reducing the need for blunt, expensive staffing responses.

- Limited Visibility Into Agent Performance and Call Drivers

AHT, adherence, and a QA score are a few KPIs that are frequently used to measure agent performance, but they don't explain why those figures appear the way they do.

- What’s really happening:

- Leaders see the result (high AHT, low FCR, variable CSAT) but not the behaviors and obstacles behind them.

- Coaching is often based on small samples or anecdotal observations.

- High performers develop their own techniques, but those don’t spread across the team systematically.

- Leaders see the result (high AHT, low FCR, variable CSAT) but not the behaviors and obstacles behind them.

- Why does this drive cost:

- Inconsistent handling creates rework and repeat calls.

- Opportunities to standardize better language, probing, and expectation-setting are missed.

- Training spends time on generic topics instead of the few high-impact behaviors that actually change outcomes.

- Inconsistent handling creates rework and repeat calls.

- What leaders need to see:

- Pattern-level insights: what do top agents do differently in similar call types?

- How often are crucial steps skipped or rushed?

- Which moments in conversations correlate with successful resolution vs. callbacks?

- Pattern-level insights: what do top agents do differently in similar call types?

QA efforts can shift from policing to enabling with a better understanding of call drivers and behaviors, and more consistent, efficient handling leads to lower costs.

- Legacy Systems Slow Down Agents and Inflate Service Costs

Even the best-trained agents can’t outrun slow tools.

- What’s really happening:

Many insurance contact centers still rely on legacy policy, claims, or CRM systems. Agents must:

- Navigate multiple screens and systems to handle basic tasks

- Repeat data entry

- Wait through system lag during live calls

- Why does this drive cost:

- Every second of system delay is counted inside AHT, and at scale that translates directly into staffing need.

- Agents put calls on hold to search and verify information, which frustrates customers and risks lower FCR.

- Workarounds add hidden labor, such as keeping manual trackers or parallel spreadsheets.

- Every second of system delay is counted inside AHT, and at scale that translates directly into staffing need.

- What leaders need to see:

- Concrete links between system steps and AHT (where exactly time is lost)

- The most painful journeys from an agent perspective

- Which legacy constraints can be mitigated with better workflows, guidance, or process changes, even before full modernization

- Concrete links between system steps and AHT (where exactly time is lost)

Modernizing core platforms is a long journey. But even before that, insurers can redesign workflows around existing tools to lower cost-to-serve and free up agent capacity.

Why This Deep Dive Matters

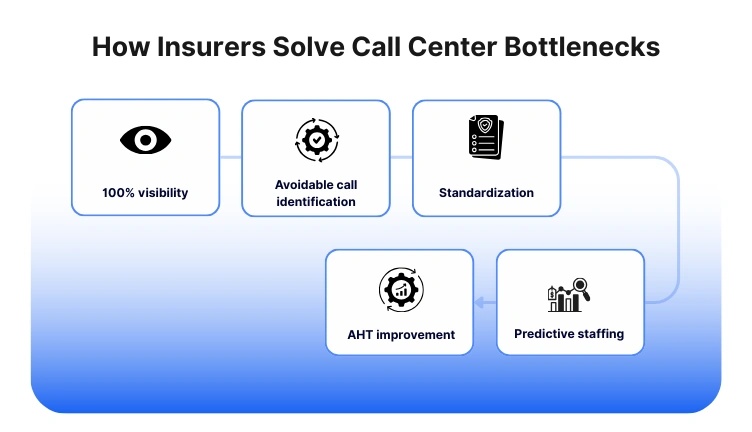

None of these problems requires immediate downsizing to solve. They require much better visibility into what’s actually happening in conversations, workflows, and systems.

Once insurers can quantify avoidable calls, understand AHT drivers, see repeat-call patterns, and pinpoint where legacy tools slow agents down, insurance call center cost reduction becomes a structured, achievable program instead of a one-time cost-cutting exercise.

Spot blockers to insurance call center cost reduction.

WHAT “GOOD” LOOKS LIKE

Most insurers don’t need a radically different contact center. They require a more precise operating picture that reflects actual conversations, identifies factors that hinder agents, and reveals what causes repeat calls and increased service costs.

Here’s what a high-performing, cost-efficient insurance contact center looks like when the bottlenecks we identified are addressed in a structured way.

You Have Full Visibility Into 100% of Conversations

Leaders in optimized environments move beyond relying on minimal QA samples, instead utilizing a comprehensive, searchable call record. This approach enables:

- The identification of real Average Handling Time (AHT) patterns categorized by call type, product line, and agent.

- The recognition of avoidable calls, such as status checks, simple clarifications, and repetitive queries.

- The early detection of recurring issues leading to repeat contacts.

- More efficient root-cause analysis during periods of claims spikes.

Enhanced visibility transforms cost reduction into a data analysis challenge rather than a staffing issue, allowing for the identification of costly workflows and their underlying reasons.

Repeat Contacts Drop Because First-Call Resolution Becomes Consistent

Understanding the root causes of repeat calls allows for systematic prevention. A robust operating model features:

- Consistent probing questions from agents.

- Clearer explanations and expectations for customers.

- Identification of risky or incomplete steps to prevent callbacks.

- Workflows that change based on common friction points in claims, FNOL, servicing, or renewals.

- Standardized language to minimize miscommunication.

Resulting benefits include:

- Increased resolution of issues on the first call.

- Reduced handle time.

- Decreased inbound call volume.

- Overall cost reduction for the insurance call center without altering headcount.

AHT Reduction Comes from Workflow Efficiency, Not Pressure on Agents

Leaders in optimized environments focus on identifying and removing structural causes of elevated Average Handling Time (AHT) rather than urging agents to work faster.

• Slow system processes are pinpointed and addressed.

• Processes are streamlined for high-volume customer journeys.

• Real-time knowledge support is provided for complex policy or claims inquiries.

• Call flow guidance ensures agents remain consistent and concise in their responses.

• Repetitive, low-complexity queries are resolved more efficiently.

• AHT decreases due to reduced friction, safeguarding customer experience (CX) and compliance while enhancing cost-effectiveness.

Staffing Decisions Become Predictive Instead of Reactive

Most insurers depend on historical averages or forecast sheets for staffing planning. More advanced models utilize patterns from actual conversations. Characteristics of an effective model include:

- Early identification of emerging call drivers (e.g., premium changes, new deductibles, documentation issues).

- Predictive signals for impending claims surges.

- Improved planning for seasonal patterns, weather events, or renewal cycles.

- Distinction between unavoidable and avoidable call volume.

This understanding helps insurers prevent costly overstaffing and reduce overtime, which are significant factors in rising contact center costs.

Coaching and Performance Management Become Targeted and Fair

Coaching effectiveness transitions from partial visibility to a model grounded in observable patterns and behaviors that improve resolution quality.

• High performers' techniques become shareable and teachable.

• Coaching emphasizes key behaviors that significantly alter outcomes.

• Feedback provided is more objective, timely, and aligned with organizational objectives.

• Agents experience a supportive coaching environment rather than a micromanaging approach.

This leads to consistent handling of customer interactions, reducing the number of escalations and repeat calls, thereby lowering operational costs predictably.

System Limitations Stop Dictating Service Quality

Insurers should design workflows that reduce system-related friction, even if they cannot update legacy platforms immediately. Strategies include:

- Pre-filling data when possible.

- Reducing duplicate steps.

- Shortening navigation paths in claims and policy systems.

- Replacing long hold-search cycles with structured guidance.

- Eliminating parallel manual trackers that contribute to additional workload.

These improvements lead to fewer delays, faster resolutions, and decreased need for increased staffing.

Cost-to-Serve Turns Into a Manageable, Measurable KPI

In high-performing centers:

- Leaders track cost-to-serve weekly, not quarterly

- They understand which workflows consume the most minutes, overtime, and callbacks

- Improvements compound because issues are fixed at the source rather than downstream

This shifts the cost conversation from “We need more people” to “We need fewer avoidable steps.” And that is where the reliable path to up to 40% cost reduction emerges.

See what effective insurance call center cost reduction looks like.

How Insurers Can Systematically Solve These Bottlenecks

Fixing avoidable calls, AHT issues, and repeat-contact loops doesn’t require a disruptive overhaul. It requires a more reliable way to see what’s happening inside conversations and workflows and then act on those insights. Most insurers begin with small, high-impact steps that steadily compound into measurable call center cost optimization.

Here’s how that transformation usually unfolds.

- Start by Analyzing 100% of Conversations, Not Just a Sample

The first shift insurers make is moving away from 1–3% manual QA sampling. To reduce cost-to-serve, they need consistent visibility into:

- Which call types inflate AHT

- Which issues generate repeat volume

- Where agents struggle with navigation or clarity

- Which behaviors correlate with successful first-call resolution

Leaders have a comprehensive, objective view of these trends thanks to automated QA and conversation analytics. This is about giving QA teams the visibility they need to identify actionable bottlenecks, not about replacing them.

Once leaders can see what’s really driving call volume and handle time, cost reduction becomes predictable.

- Build a Clear Map of Avoidable Calls and Upstream Fixes

Many of the highest-volume calls in insurance are preventable: unclear premium explanations, status checks, missing documentation, or timelines customers don’t fully understand.

A structured root-cause breakdown helps insurers:

- Quantify avoidable vs. unavoidable traffic

- Identify messaging gaps that trigger inbound calls

- Spot failure points in claims and FNOL

- Reduce the load on frontline teams without reducing staff

Convin is a natural fit in this situation, but it doesn't promote the product; instead, it provides teams with the clarity they need to address previously undetectable problems.

- Standardize Resolution Behaviors That Improve FCR

When insurers identify the conversational moments that lead to successful resolutions, they can standardize them across teams.

This typically includes:

- Better probing questions

- Clearer expectation-setting

- Standard phrasing for complex coverage explanations

- Fewer holds and transfers

- Automatic reminders for critical steps agents often miss

Instead of pressuring agents to reduce Average Handle Time, insurers coach agents toward higher First Call Resolution, which naturally lowers AHT and repeat volume, rather than putting pressure on them to reduce Average Handle Time.

The goal is consistency, not control. Better conversations reduce workload for everyone.

- Surface Workflow and System Friction That Drive Up AHT

Some AHT drivers have nothing to do with conversation quality. They stem from:

- Slow or fragmented legacy systems

- Repetitive data-entry loops

- Unclear workflows in claims or policy servicing

- Navigational dead ends that force holding patterns

Automated QA helps operations teams identify issues promptly, allowing them to focus on fixes that have a real-world impact. Minor workflow changes, like eliminating repetitive tasks or streamlining navigation, can decrease handle time without altering staff numbers.

- Use Pattern Insights to Prepare for Claims Surges

During claims spikes, insurers often resort to expensive overtime or temporary staffing because they don’t have clear triggers showing why call volume is rising.

With conversation-level insights, insurers can:

- Identify early signs of surge drivers (e.g., document requests, FNOL questions)

- Predict what category of calls will grow and when

- Fine-tune staffing instead of overstaffing

- Prioritize self-service or outbound messaging where it matters most

This reduces the operational burden during high-stress periods and brings more stability to cost-to-serve.

- Make Coaching Targeted, Fair, and Continuous

Because automated QA analyzes every interaction, coaching stops being subjective or based on limited samples.

Leaders can see:

- Where new agents consistently struggle

- What top performers do differently

- Which behaviors directly influence FCR and repeat calls

- When process gaps, not agent skill, are the real culprits

This makes coaching less about correction and more about support. Agents receive actionable, context-specific guidance, improving consistency without adding more layers of manual oversight. Coaching becomes a lever for stability, not a pressure point.

- Track Cost-to-Serve as a Live Metric, Not a Retrospective One

Insurance companies can now measure cost drivers on a weekly basis rather than a quarterly basis, thanks to a modern operating model.

This includes live visibility into:

- AHT trends by workflow

- Repeat-call rates and their root causes

- Avoidable-call volume and progress

- Claims-related surges and their triggers

- Agent efficiency patterns

- Process resolution quality

Insurance call center cost reduction is not a one-time cost-cutting initiative but rather the natural result of resolving operational bottlenecks once insurers use these insights to inform decisions.

Learn how insurers approach call center cost reduction.

This blog is just the start.

Unlock the power of Convin’s AI with a live demo.

How Insurance Companies Reduce Call Center Costs by 40% Without Downsizing

Cutting operational costs in a contact center isn’t about squeezing agents or eliminating roles. It’s about removing friction, reducing avoidable volume, and strengthening first-call resolution. This playbook outlines the actions taken by high-performing insurance organizations once they achieve full visibility into conversations and workflows.

These procedures are feasible at any scale because they are repeatable, workable, and compatible with legacy systems.

Step 1: Analyze 100% of Calls to Identify Cost Drivers

Because manual QA only covers a small sample, the majority of insurers only have partial visibility. Even at a high level, reviewing each interaction helps leaders understand:

- AHT patterns by call type

- Which workflows generate the most repeat contacts

- Avoidable vs. unavoidable call volume

- Where system drag or knowledge gaps slow agents down

This step ensures that call center cost optimization targets the right problems, not just symptoms.

Step 2: Break Down Avoidable Call Categories and Fix Upstream Triggers

Insurers can begin removing avoidable volume once call drivers are identified, which is frequently the quickest way to cut costs.

Typical high-impact categories include:

- unclear premium or coverage explanations

- status checks caused by delayed notifications

- missing documents or incomplete guidance

- repetitive policy renewal queries

- claim-stage confusion and next-step uncertainty

Upstream fixes may involve rewriting templates, adding proactive communication, or standardizing agent phrasing.

Step 3: Standardize High-Impact Behaviors to Lift FCR

AHT and repeat calls are consistently decreased by raising First Call Resolution (FCR). Finding the unique behaviors of top-performing agents and implementing them throughout the team are crucial.

This often includes:

- structured probing questions

- clearer timeline/expectation setting

- resolving the reason behind the call, not just the immediate question

- reducing avoidable transfers

- ensuring complete resolution steps are followed

With consistency, agents spend less time clarifying and more time resolving.

Step 4: Remove Workflow Friction That Inflates AHT

Operational teams should identify which process steps consistently cause delays (hold time, duplicate data entry, multiple system hops) and prioritize workflow fixes.

Examples of “small but high-impact” improvements include:

- consolidating knowledge into a single searchable format

- reducing redundant fields in claims or policy servicing tools

- streamlining steps for high-volume journeys like FNOL or renewals

- clarifying scripts around complex coverage explanations

AHT comes down naturally when friction is removed.

Step 5: Prepare for Claims Surges With Pattern Intelligence, Not Overtime

Instead of relying on reactive staffing, insurers can use patterns from recent conversations to forecast:

- expected claim types

- documentation gaps

- hold-time pressure points

- surge triggers (weather, seasonal cycles, rate changes)

This enables more precise staffing plans and reduces the need for overtime or temporary workers.

Step 6: Make Coaching Targeted and Evidence-Based

Coaching becomes more effective when it focuses on:

- recurring errors

- missed steps

- inconsistent explanations

- behaviors correlated with low FCR

- segments of calls with long handle time

This improves overall handling quality without raising labor costs by changing coaching from general feedback to targeted improvement.

Step 7: Treat Cost-to-Serve as a Live KPI

Rather than waiting for quarterly reports, high-performing insurers track cost-to-serve continuously.

Useful weekly view:

- AHT by workflow

- repeat-call rate

- avoidable-call share

- agent-level efficiency trends

- claims surge indicators

- resolution completeness metrics

This real-time lens helps leaders correct issues while they are still small and inexpensive to fix.

See insurance call center cost reduction in action.

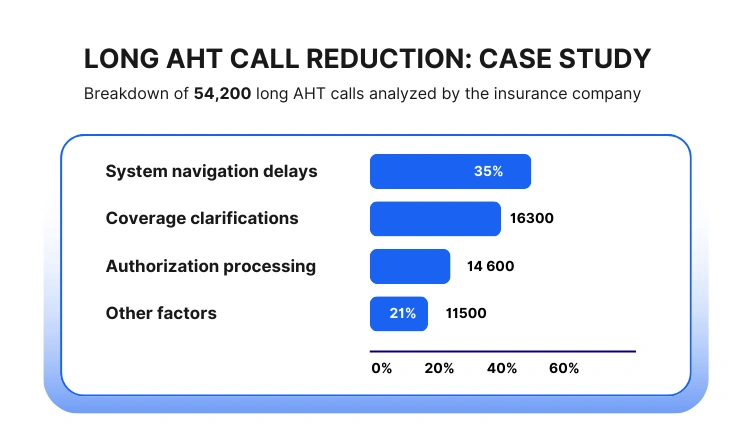

Convin Case Study 1: Long AHT Reduction

An exceptional US health insurer noticed rising operational costs tied to extended Average Handle Time (AHT). Although staffing had grown year over year, service levels did not improve. Leadership suspected workflow and knowledge friction but lacked visibility into the exact drivers.

What the Analysis Found

Across 54,200 calls flagged as having above-target AHT, the AI-assisted breakdown revealed the following distribution:

Insights That Shifted Decision-Making

- Over one-third of long calls stemmed from agents switching between legacy apps, not from conversation complexity.

- Nearly 30% were caused by unclear benefit explanations that varied by agent, leading to long back-and-forth interactions.

- System friction accounted for a smaller percentage but had an outsized impact because it prolonged hold times and increased customer frustration.

Actions Taken

- Consolidated reference material into a simplified, searchable knowledge layer.

- Provided consistent phrasing templates for benefit and coverage explanations.

- Flagged backend system modules are causing the longest delays and have introduced interim workarounds until the modernization project is completed.

Outcome (6 weeks)

- 18% reduction in AHT for the top three high-volume call types.

- 11% drop in total handling time across the service desk.

- Noticeable reduction in overtime requirements during peak enrollment season.

This case illustrates how insurers can achieve meaningful call center cost optimization by targeting workflow-level friction rather than relying on headcount increases.

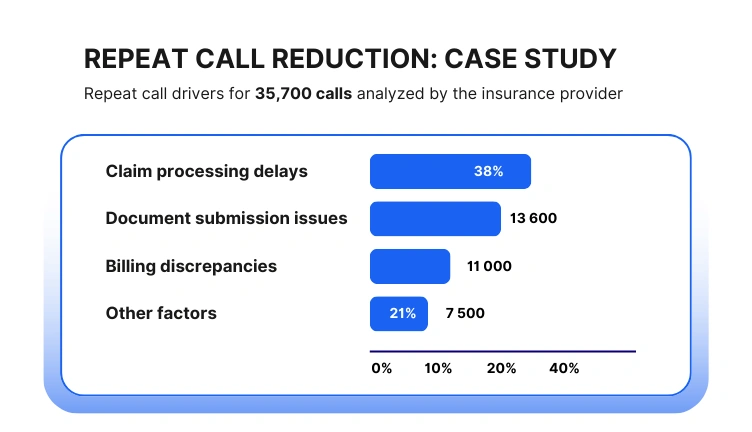

Convin Case Study 2: Repeat Call Reduction

A property & casualty insurer in APAC faced steadily increasing repeat contacts within 10 days of the initial call, especially around claims and policy servicing. Traditional QA reviewed fewer than 2% of calls, leaving leaders uncertain about the true causes.

What the Analysis Found

Out of 31,800 detected repeat-call cases, the categorization looked like this:

What This Revealed

- Nearly 1 in 3 repeat calls were triggered by vague or incomplete explanations during the initial conversation.

- A significant 24% came from first-call resolutions marked “completed” even though customers still had pending questions or missing documents.

- The insurer’s email/SMS updates did not match the timing or language used in agent conversations, causing customers to seek clarification.

Actions Taken

- Standardized claim-status explanations and next-step phrasing across teams.

- Introduced reminders for agents when key steps (document checklist, settlement timelines) were skipped.

- Improved synchronization between CRM updates and outbound notifications.

Outcome (8 weeks)

- 27% reduction in repeat-call volume, especially in early claim-cycle segments.

- Higher FCR scores for four major call types.

- Stabilized staffing needs during monsoon-related claim surges, avoiding additional temporary hiring.

This case shows how insurers can meaningfully lower cost-to-serve by addressing the clarity, consistency, and follow-through gaps that fuel repeat volume.

Outcome: A Predictable Path to 40% Cost Reduction

Once insurers have visibility into every conversation, consistent resolution behaviors, and friction-free workflows, they experience:

- fewer repeat contacts

- shorter handling times

- more predictable claims surges

- less reliance on overtime

- reduced operational load without reducing staff

This is how contact centers achieve meaningful insurance call center cost reduction without compromising service or morale.

Apply a proven insurance call center cost reduction playbook.

WRAP-UP: A Clear Path to Lower Costs Without Losing Capability

Insurance contact centers don’t need to rely on downsizing to control costs. They require a better comprehension of the factors that truly influence volume, time management, and repeat business, as well as the capacity to address those problems at their root.

When leaders can see these patterns across 100% of conversations, cost reduction stops being a reactive budgeting exercise and becomes a continuous operational discipline.

The data from industry benchmarks, anonymized cases, and workflow-level insights all point to the same conclusion:

Most of the pressure on AHT, repeat calls, and staffing demand comes from inefficiencies - not from a lack of people.

When insurers remove friction, standardize communication, and build consistency around resolution quality, they unlock a more stable and predictable operating model.

Teams feel less overwhelmed, customers get clearer answers, and the organization gains meaningful cost improvements without compromising service.

Reducing cost-to-serve by up to 40% is not an ambitious goal; rather, it is the result of numerous small, focused fixes implemented with discipline and visibility.

If you want a clearer view of what’s driving your AHT, repeat calls, and cost-to-serve, you can watch a short demo that shows how conversation insights surface these patterns without disrupting your current workflows.

Frequently Asked Questions

1. How does insurance call center cost reduction impact customer satisfaction?

When insurers reduce avoidable calls and improve first-call resolution (FCR), customers spend less time waiting or calling back. This typically improves CSAT while lowering overall cost-to-serve.

2. Can insurance call centers reduce costs without outsourcing?

Many insurance contact centers achieve call center cost optimization internally by fixing AHT drivers, repeat calls, and workflow inefficiencies without outsourcing or downsizing teams.

3. What role does AI play in insurance contact center efficiency?

AI helps insurers analyze 100% of calls, identify repeat-call drivers, and surface AHT bottlenecks. This improves insurance contact center efficiency by enabling faster, data-backed operational decisions.

4. How do insurers measure cost-to-serve in call centers?

Cost-to-serve is measured by combining staffing costs, AHT, repeat-call rates, and volume by call type. Leading insurers track this weekly to guide continuous call center cost optimization.

5. Are call center cost savings sustainable without reducing headcount?

Insurance call center cost reduction is sustainable without layoffs when workflow friction is eliminated, and repeat contacts are avoided.

.avif)

.avif)