Insurance contact center compliance has stopped being a back-office checkbox. For modern insurance leaders, it is now a board-level risk affecting revenue, brand trust, and regulatory viability.

Many insurance contact centers face challenges not due to a lack of intention, but because compliance operations have developed in silos. Call recordings are stored in separate systems, quality audits are conducted using spreadsheets, and regulatory reports are produced manually, leading to inefficient data assembly when compliance inquiries arise.

This fragmentation leads to unseen risks, as non-compliant calls are overlooked until it's too late. Audit preparation becomes a reactive process, and reporting shifts from routine to an urgent scramble, undermining continuous compliance efforts.

The data reveals that over 60% of insurance companies encountered compliance-related issues within the last two years, indicating significant regulatory gaps in risk management.

Additionally, industry dashboards automating analytics and reporting can enhance compliance by approximately 30% and accelerate audit preparation by up to 50% versus manual methods.

Regulatory expectations are also rising. Insurance regulators are no longer satisfied with policies on paper. They expect documented evidence. Clear call records. Consistent disclosures. Verifiable audit trails. The burden of proof now sits with the insurer.

CEOs and compliance leaders face challenges due to fragmented systems, which undermine confidence despite having various tools, processes, and teams in place.

This gap between perceived compliance and provable compliance is where most insurance contact centers start to fall apart.

Explore how a compliance-ready contact center operates in real time.

Why Insurance Contact Center Compliance Keeps Falling Apart

Insurance contact center compliance breaks down in predictable ways. Not because teams are careless, but because the operating model was never designed for today’s scrutiny.

A compliance-ready contact center needs provable control across every interaction. Most contact centers still run on disconnected workflows that make proof slow, manual, and inconsistent.

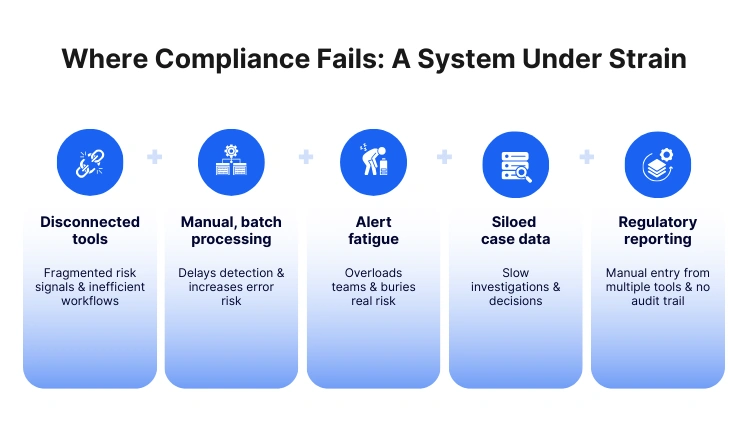

Fragmentation is the real failure point

In many insurers, insurance call recording compliance sits with IT or a telecom vendor. QA sits with operations. Risk and compliance owns policy, but not the evidence. The result is scattered ownership and scattered data.

What this looks like on the ground:

- Recordings stored separately from CRM and disposition data

- QA forms in spreadsheets or a standalone tool with limited coverage

- Audit samples are chosen manually, often after an issue escalates

- Compliance reporting is assembled by pulling exports from multiple systems

When evidence is fragmented, contact center regulatory compliance insurance becomes a monthly or quarterly scramble, not a daily posture.

McKinsey flags this exact blocker across contact centers: hurdles in connecting systems and data slow down adoption of new workflows and make transformation harder than it should be.

Manual QA means low coverage and delayed detection

Most centers still review a small fraction of calls. That creates a dangerous blind spot for insurance call monitoring and audit compliance.

Common failure patterns:

- Script adherence is checked on too few interactions to be meaningful

- High-risk moments are missed, especially product disclosures and consent

- Issues get discovered only after a complaint, cancellation, or regulatory query

- Coaching focuses on outcomes, not compliance evidence

Your compliance confidence is essentially an assumption if your QA coverage is not scalable.

IRDAI expectations demand evidence, not intention

For IRDAI compliance for insurance call centers, the guidelines around distance marketing make it clear that insurers and their partners must treat voice interactions as regulated records.

Key requirements that trip teams up operationally:

- Telemarketers are expected to maintain and preserve call recordings, and those records can be inspected by the Authority.

- Insurers must use standardized scripts with required disclosures, approved by compliance, and filed under “Use & File” procedures.

- Consent is not implied. Telephonic solicitation should proceed only after explicit client consent to continue.

- Insurers must preserve a voice or electronic record of the full solicitation-to-sale process for a defined retention period, with digitization, encryption, and easy retrieval expectations.

This is the practical challenge: insurance contact center compliance is no longer about having the right policy. It is about producing call-level proof fast.

“Recording exists” is not the same as “recording is compliant”

A lot of teams believe they are covered because they record calls. But insurance call recording compliance is bigger than storage.

Auditors and internal risk teams typically care about:

- Completeness: was the full interaction captured, including transfers

- Integrity: is the record tamper-resistant and traceable

- Retrieval: can you find the exact call quickly with context

- Linkage: can you connect the recording to the agent, script version, disposition, and customer outcome

- Retention: can you demonstrate that retention rules are consistently applied

If recordings are not searchable, linked, and auditable, a compliance-ready contact center is hard to defend under pressure.

Reporting and audit trails are built too late

The final breakpoint is reporting. Most compliance reporting is built backwards. Teams start with the audit request, then work back through systems to assemble evidence.

That leads to:

- Inconsistent metrics across teams and vendors

- Gaps in audit trail continuity

- High dependence on manual exports and individual SMEs

- Slow response timelines during regulatory scrutiny

And that is the core reason insurance contact center compliance keeps falling apart. The work is reactive, the data is scattered, and proof is hard to produce when it matters most.

However, insurance call recording compliance is more extensive

What Today’s Insurance CEOs Expect From a Compliance-Ready Contact Center

Modern insurance CEOs no longer view compliance as a downstream operational concern. They see insurance contact center compliance as a direct indicator of enterprise risk, governance maturity, and brand credibility. Expectations have shifted from intent to evidence.

First, CEOs expect continuous compliance visibility, not quarterly snapshots. They want to know whether regulatory risk exists today, not after a complaint or an audit notice.

A compliance-ready contact center must surface compliance signals across every interaction, every agent, and every campaign. When compliance insights are delayed or sampled, confidence drops.

Second, CEOs expect audit readiness by default. In a regulated industry, audits are not exceptions. They are inevitable.

Leadership expects that evidence for contact center regulatory compliance insurance can be produced quickly, consistently, and without internal escalation. That includes access to call recordings, audit trails, QA outcomes, and disclosure proof without dependency on manual data pulls.

Third, CEOs expect regulatory alignment without operational drag. Meeting IRDAI compliance for insurance call centers should not slow growth or customer experience.

Leaders want compliance embedded into daily workflows so agents, QA teams, and compliance teams operate from the same standard. If compliance feels like an external checkpoint rather than a built-in process, it signals systemic weakness.

Fourth, CEOs expect accountability with traceability. When issues arise, leadership wants clarity.

Which interaction failed?

Which agent behavior caused the gap?

Which script or disclosure version was used?

This level of traceability depends heavily on strong insurance call monitoring and audit compliance and tightly linked call data.

Finally, CEOs expect confidence under scrutiny. Whether it is a regulator, board member, or external auditor, leadership wants assurance that the organization can stand behind its processes. A compliance-ready contact center is one where compliance conversations are calm, factual, and backed by evidence rather than assumptions.

The Must-Have Capabilities of Insurance Call Center Compliance Software

A strong insurance call center compliance software foundation is what enables these CEO expectations to become operational reality. Without it, insurance contact center compliance remains reactive and fragile.

- Centralized and compliant call recording

At the core lies insurance call recording compliance. This goes beyond capturing audio. Call recordings must be complete, tamper-resistant, searchable, and retained according to regulatory guidelines. Recordings should be consistently linked to agent identity, customer context, and interaction outcomes. Without this linkage, recordings exist but do not protect the business.

- Scalable call monitoring and audit coverage

Effective insurance call monitoring and audit compliance require scale. Reviewing a small sample of calls cannot support regulatory confidence. Compliance software must enable broader monitoring across interactions, highlighting risk patterns early. This ensures that deviations from approved scripts, disclosures, or consent requirements are detected before they escalate.

- Built-in regulatory workflows

For contact center regulatory compliance insurance, workflows matter. Compliance checks should not live outside the system. Disclosure validation, consent confirmation, and policy adherence need to be part of the same operational flow as call handling and QA. This alignment reduces reliance on memory, manual checks, and post-call correction.

- IRDAI-aligned audit trails and reporting

Meeting IRDAI compliance for insurance call centers depends on structured audit trails. Compliance software should automatically maintain logs that show when calls occurred, how they were handled, which scripts were used, and how long records are retained. Reporting should be consistent, standardized, and easily reproducible under audit conditions.

- Single source of compliance truth

Finally, a compliance-ready contact center depends on unification. Call recordings, QA scores, monitoring insights, and audit reports must live in one system. Fragmentation creates doubt. A single source of truth creates confidence. This is what allows leadership to move from hoping they are compliant to knowing they are.

When these pillars are missing or partially implemented, insurance contact center compliance weakens. When they are present and connected, compliance becomes a durable operating advantage rather than a recurring risk.

Now check whether leadership can see compliance without asking for a report.

This blog is just the start.

Unlock the power of Convin’s AI with a live demo.

IRDAI Compliance for Insurance Call Centers: What Auditors Actually Check

When auditors assess IRDAI compliance for insurance call centers, they are not judging effort. They are checking whether your insurance contact center compliance is provable, repeatable, and consistent across calls, teams, and vendors. The fastest way to fail is to show policies without evidence.

Here is what IRDAI-aligned audits typically zero in on.

1) Proof of explicit consent and compliant call openings

Auditors look for clear evidence that telephonic solicitation proceeds only after the customer explicitly agrees to continue. If your process cannot consistently capture this, contact center regulatory compliance insurance becomes hard to defend.

They also check whether calls follow a standardized introduction process that makes it obvious the purpose is insurance solicitation, including identity disclosure and language choice.

Why this matters for buyers: if consent and opening disclosures are not consistently captured, the rest of the call can become irrelevant from a compliance standpoint.

2) Standardized scripts, and proof agents followed them

Auditors often ask two things:

- Do you have approved standardized scripts for product presentation and disclosures

- Can you prove calls were conducted in accordance with those scripts

The guideline expects standardized scripts and indicates submission for approval before use.

This is where many insurance call center compliance software evaluations begin. CEOs want to know that script governance is not just a document but something operationally enforceable through monitoring and audit workflows.

3) Call recording disclosures and customer access rights

IRDAI-aligned checks typically include whether callers inform customers that the call is being recorded and whether customers can request a voice copy within a specified window.

This is a direct pressure point for insurance call recording compliance. It is not enough to have recording enabled. You need:

- Proof the recording disclosure happened

- The ability to retrieve and share records when required

- Confidence that records are complete and correctly mapped to the policy or risk commencement

4) Preservation, integrity, and retrieval of the full sale journey

Auditors look beyond “one recording.” They look for an inalterable, easily retrievable record of the entire process from solicitation through sale, preserved through the policy term. The guideline also calls out digitization and encryption for voice and electronic records.

This is where insurance contact center compliance breaks when data is scattered. Even if you have recordings, if you cannot retrieve the right evidence fast, it becomes a compliance risk during scrutiny.

Also, because insurers handle sensitive customer and financial data, auditors increasingly tie this back to security and access controls. IRDAI’s Information and Cyber Security Guidelines push insurers toward stronger governance, controls, and protection of information assets.

5) Monitoring and verification coverage expectations

Auditors are highly attentive to whether monitoring is structured and not symbolic. The distance marketing guideline describes:

- Monitoring calls live by listening to at least 5% as they happen

- Verifying at least 10% of calls leading to sales for compliance, with observations preserved for at least three years

- Making verification calls to a minimum of 20% of policyholders purchasing via distance mode every month, using a standardized script, with records preserved for at least three years

This directly drives the need for scalable insurance call monitoring and audit compliance. If your compliance approach relies on manual sampling and ad hoc checks, meeting coverage expectations becomes expensive and inconsistent.

6) Traceable audit trails across people, process, and outcomes

Finally, auditors expect traceability.

Who called?

What product was discussed?

Which script version was applied?

Whether disclosures were made.

What did the customer respond?

What happened after the call?

In a true compliance-ready contact center, these are not separate activities. They are linked. That linkage is exactly what most teams cannot produce quickly when operating across multiple tools and vendors.

Why Traditional Call Center Tools Can’t Support Compliance at Scale

Most legacy stacks were built to run operations, not to prove insurance contact center compliance under regulatory scrutiny. They create activity, but not defensible evidence.

Here is how they fail in practice.

1) Point solutions create compliance gaps between systems

A recorder stores audio. A QA tool stores scores. A CRM stores outcomes. A BI tool stores reports. None of them share the same truth by default.

That means contact center regulatory compliance insurance becomes a stitching exercise:

- Matching call IDs to policies and customers

- Reconciling QA results with recordings

- Rebuilding timelines during an audit

A compliance-ready contact center cannot rely on stitching.

2) Call recording systems are not built for compliance proof

Legacy recording setups often answer “did we record,” but not “is it compliant.”

Common gaps in insurance call recording compliance with legacy tools:

- Hard retrieval and poor searchability during audits

- Weak linkage to agent identity, campaign, and policy outcome

- Limited integrity controls and incomplete audit trails

- Retention policies applied inconsistently across vendors and sites

You end up with recordings that exist but cannot reliably support IRDAI audit expectations.

3) Manual QA cannot scale to IRDAI-aligned coverage

When monitoring is spreadsheet-driven or reliant on small QA teams, coverage stays low. But IRDAI expectations around monitoring, verification, and record preservation make low coverage risky.

This is where decision-makers start evaluating insurance call center compliance software seriously. They need monitoring that scales without multiplying headcount.

4) Reporting is reactive and fragile

Legacy reporting tends to be built after the fact:

- Exports from multiple tools

- Manual pivot tables

- Different definitions across teams

- No consistent audit trail for how metrics were produced

When an audit happens, the organization spends time proving the report, not proving compliance.

5) Security and access controls are often bolted on

As insurers strengthen data security practices under IRDAI cybersecurity expectations, access control, encryption, and governance become more tightly scrutinized.

Legacy stacks often treat security as an IT layer rather than a compliance requirement that spans recordings, QA artifacts, reports, and audit logs. That is a mismatch for a compliance-ready contact center.

Legacy tools fail because they create operational output without compliance-grade evidence. In today’s environment, insurance contact center compliance is judged by how quickly and reliably you can produce proof across call recordings, monitoring, verification, and audit trails.

That is why buyers shift from “tools that help agents talk” to insurance call center compliance software that can sustain insurance call monitoring and audit compliance, support IRDAI compliance for insurance call centers, and keep the contact center audit-ready every day.

Identify where manual handoffs still exist in your compliance flow.

How Convin Creates a Single Source of Truth for Insurance Compliance

Insurance leaders do not ask whether compliance matters at a stage. They are asking whether their systems can stand up to scrutiny. This is where Convin’s approach to insurance contact center compliance becomes materially different. It is built to replace fragmentation with clarity.

Convin is designed as insurance call center compliance software that unifies evidence, monitoring, and reporting into one operational layer. The goal is simple. Make compliance provable at any moment, not reconstructable after the fact.

One unified system for regulated voice interactions

Convin centralizes call data that usually lives across multiple tools. Insurance call recording compliance, quality evaluations, monitoring insights, and audit logs are all tied to the same interaction record.

This matters because contact center regulatory compliance insurance depends on linkage. Auditors do not want isolated artifacts. They want context. With Convin, every call recording is automatically connected to the agent, script version, customer journey stage, and QA outcome. This creates continuity instead of patchwork.

Compliance monitoring that scales without manual overhead

Convin strengthens insurance call monitoring and audit compliance by moving beyond small samples. Instead of relying only on manual QA, compliance teams get broad visibility across interactions.

This enables:

- Early identification of disclosure and consent gaps

- Consistent enforcement of approved scripts

- Ongoing validation of regulatory adherence, not episodic checks

For leadership, this reduces dependency on assumptions. Compliance posture is visible, measurable, and continuously improving.

Built to support IRDAI audit expectations

IRDAI compliance for insurance call centers requires more than recording calls. It requires structured evidence. Convin supports this by maintaining clear audit trails across the solicitation and sale process.

Key compliance outcomes supported:

- Verifiable call recording disclosures

- Proof of standardized script usage

- Traceable consent capture

- Secure storage and retention aligned with regulatory timelines

- Fast retrieval of historical records during audits

Because evidence is already organized, audits become a verification exercise rather than a reconstruction exercise.

Consistent reporting from a single source of truth

One of the biggest compliance risks is inconsistent reporting. Different teams using different numbers erodes confidence quickly.

Convin solves this by acting as the single source of truth for insurance contact center compliance reporting. Compliance metrics, monitoring outcomes, and audit evidence are derived from the same data foundation. This consistency is critical for internal governance, board reviews, and regulatory discussions.

A compliance-ready contact center by design

A compliance-ready contact center is one where compliance is not an external layer. It is embedded into daily operations. Convin aligns agents, QA teams, and compliance leaders around the same system, the same standards, and the same evidence.

For buyers, the value is not theoretical. It is operational confidence. The ability to answer regulatory questions quickly. The ability to demonstrate control without scrambling. The ability to move from reactive compliance to sustained assurance.

See what changes when compliance evidence lives in one system.

Insurance contact center compliance is no longer defined by policies, intent, or effort. It is defined by evidence. For modern insurers, the real risk is not noncompliance in isolation but the inability to prove compliance consistently and quickly when scrutiny arrives.

As regulatory expectations rise, especially around IRDAI compliance for insurance call centers, fragmented systems, manual audits, and reactive reporting continue to expose gaps. A compliance-ready contact center is one where call recording, monitoring, audits, and reporting work together by default, not through last-minute coordination.

The difference between confidence and uncertainty comes down to having a single source of truth for insurance contact center compliance. One that supports regulatory requirements, scales with operations, and holds up under audit pressure.

Schedule a Convin demo to experience how call recording, monitoring, and audit readiness come together in one system built for insurance compliance.

this

Frequently Asked Questions

1. What is insurance contact center compliance in outsourced call centers?

Insurance contact center compliance applies equally to in-house and outsourced teams. Insurers remain accountable for call recording, monitoring, disclosures, and audit trails, even when third-party vendors handle customer conversations.

2. How long should insurers retain call recordings for regulatory compliance?

Insurance call recording compliance typically requires retaining voice records for the full policy term and additional years as mandated by regulators like IRDAI, with secure storage and easy retrieval during audits.

3. Does insurance call center compliance software replace manual audits completely?

Insurance call center compliance software reduces reliance on manual audits by scaling monitoring and evidence capture, but compliance teams still validate outcomes and handle regulatory interpretation.

4. How does contact center regulatory compliance insurance affect customer experience?

Strong contact center regulatory compliance in insurance improves trust by ensuring consistent disclosures, accurate policy explanations, and fewer post-sale disputes or complaints.

5. What defines a compliance-ready contact center across insurance channels?

A compliance-ready contact center centralizes call recordings, monitoring, QA, and audit reporting across voice, campaigns, and vendors, enabling consistent insurance contact center compliance at scale.

.avif)

.avif)